The Great War and the Great Bull Market

The Great War and the Great Bull Market

In 1859, Edwin (Colonel) Drake successfully completed the first modern oil well in American history. After weeks of trudging through bedrock at a tantalizing rate of three feet per day, Drake’s steam-powered drill bit finally reached its maximum depth of 69.5 feet on August 27th. The following day, a member of the Seneca Oil Company visited the site of the company’s speculative venture and was pleased to find crude oil bubbling up to the surface. Despite producing upwards of 15 barrels of oil a day, Drake’s first well never ended up turning a profit. Nevertheless, the Seneca Oil Company’s revolutionary project ignited the first great oil boom in American history.

The steam-powered drilling technique that Colonel Drake pioneered quickly spread throughout Pennsylvania. Simultaneously, hundreds of refineries sprang up across America to meet the nation’s growing demand for kerosene. Between 1859 and 1865, the price of crude increased eightfold. Unfortunately, the euphoria was short-lived. After climbing as high as $8.06/bbl in 1864, the nascent market for crude oil took a nose dive. By 1868, drillers were selling their oil for a mere $2.5/bbl. Despite several short-lived price spikes throughout the 1860s and early 70s, the oil market had entered the first of many cyclical downturns.

The problem was simple: the oil market was oversupplied. The demand for kerosene, though steadily increasing, could not keep up with the astronomical increase in oil production and refining. As John D. Rockefeller recalled in his later career, everyone from “the butcher, the baker, and the candlestick-maker began to refine oil.” To solve the problem of oversupply, Rockefeller’s Standard Oil began consolidating the industry. After a two-decade serial acquisition campaign, Standard Oil controlled over 90% of America’s refinery output in 1890. For the next 25 years, a combination of Standard Oil’s outsized purchasing power and sustained capital investment in new oil fields glutted the oil drilling business. Despite their rapidly increasing production base, oil producers faced a half-century of misery. Looking back on the 1860s oil boom and the late 19th century’s oil bust today, it becomes clear that these were no black swan events. Indeed, the period’s triumphant highs and ruinous lows would foreshadow the following 120 years of volatility in the oil trade.

Despite the monumental achievements of the oil industry between 1859 and 1890, the market dynamics of the period bear little resemblance to the present. Notwithstanding their primitive drilling techniques and a poor understanding of petroleum economics, wildcatters in the 19th century exploited every field they could find, no matter how uneconomical. Meanwhile, demand for crude oil was primarily limited to the production of kerosene at a time when demand was relatively stagnant. A far fetch from today’s multinational trillion-dollar industry, the oil market in the 19th century and its abnormal dynamics provide few clues to forecasting petroleum’s future in the 2020s. Rather, to understand oil’s future this decade, one needs to look no further than the period between 1914 and 1920.

By the start of World War 1, everything had changed in the world of petroleum. The rotary drilling rig had taken over in what was now an increasingly global oil market. Standard Oil, though still a wildly profitable enterprise, had been broken up into regional businesses by an antitrust suit brought against it in 1906. Simultaneously, the demand for oil products was increasing exponentially with the adoption of internal combustion engines and oil-powered ships. Between 1916 and 1918 alone, the number of cars in use nearly doubled. The looming threat of war in Europe also sparked a new emphasis on energy security for the major powers. The British government accordingly took a majority stake in the Anglo-Persian Oil Company to ensure adequate supplies from the Middle East. Likewise, the Wilson Administration created the Fuel Administration to supervise US exports to the Allies. To governments and businessmen alike, it was becoming clear that petroleum represented both the present and the future.

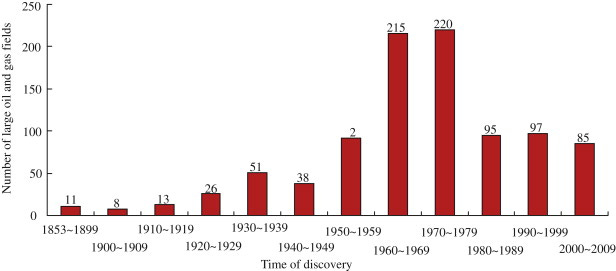

As the demand picture for petroleum shined bright during the Great War, a large panic set in over the future of oil supplies. In 1917, the Allies faced a significant oil crunch. Britain and France were forced to strictly ration oil consumption in light of significant wartime shortages. Even the US, despite producing roughly 335 million barrels of oil in 1917, was forced to import oil from Mexico that winter. Layered on top of the short-term supply challenges was a broader worry that “peak oil” supply had been reached. In 1919, the chief geologist at the United States Geological Survey proclaimed that “the peak of (oil) production will soon be passed, possibly within 3 years.” Similarly, in 1921, the President of the Colorado School of Mines predicted that “the average middle-aged man of today will live to see the virtual exhaustion of the world’s supply of oil from wells.” Concerns about peak oil were not unwarranted. From 1900 to 1920, the number of new proved reserves was not keeping up with the yearly growing demand for petroleum. This helped accentuated the fear throughout the late 1910s and early 1920s that the world was rapidly running out of oil.

Emerging from a half-century glut where the predominant worry was oversupply, the price of oil tripled from $.81/bbl in 1914 to $3.07/bbl in 1920. The rapid rise in crude prices was met with a swift supply response. With future demand all but certain to rise while future supply was becoming increasingly uncertain, oil companies embarked on massive campaigns to find new fields. For the most part, they were successful. From 1900 to 1920, only 21 new major oil and gas fields were discovered. During the 1920s alone, companies discovered 26 new fields. As a result of both new geological discoveries and further advancements in extraction technologies, U.S. oil production increased fivefold. The volume of new production was so large that, despite an exponential rise in demand for petroleum products throughout the 1930s and 40s, the petroleum market once again became oversupplied. Consequently, oil prices remained under $1.50/bbl until after the Second World War.

So what does the period following World War I have to tell us about oil markets today? For one, nearly all the key drivers of oil’s rise in price during the 1910s seem to be reversed today. Whereas a future of internal combustion engines spanning from cars to planes to ships was viewed as all but a certainty during the Great War, today their future is severely in doubt. So far as the modern story goes, gasoline-powered cars are entering a terminal decline, airplanes will run on biofuels, and ships on hydrogen. The optimism about a growing world economy that will demand more energy in aggregate is also fading. We are long past the early 2000s when commodity analysts viewed China’s continued expansion, and thus increasing demand for petroleum, as a certainty.

More than just the drastically differing demand outlooks between the 1910s and today, a great divergence has formed between each period’s consensus view of oil supply. The fears about peak oil supply that hung over the 20th century have largely evaporated. King Hubbert’s infamous model, which predicted a terminal decline in US oil production beginning in 1965, was irrevocably broken in the 2000s. After the unconventional revolution allowed producers to extract oil from previously unexploitable shale rock, geologists have estimated that over 8 trillion barrels of oil are trapped in the world’s shale resources. That is approximately 80 years of supply at current rates of consumption. All the while, dire predictions of decreasing oil production in Saudi Arabia, put forth in books like Matthew Simmons’ Twilight in the Desert, have appeared to be incorrect. Unlike in the 1910s, when producers were scouring the globe to find new exploitable resources, long-cycle investments in oil production are, for the most part, viewed as short-sighted and uneconomical. Persistent fears of oversupply in the past few years have, for the first time in history, led to a multi-year decrease in global capital investment in oil and gas.

One important similarity exists between the 1910s and today: both periods sparked a renewed interest in energy security. Similar to fears of an unstable Russian supply following the Revolution of 1917, Russia’s current invasion of Ukraine, and the resulting energy shock in Europe, have demonstrated the importance of having dependable energy suppliers. The notable difference between each period’s respective concerns over energy security is the response they elicited from policymakers. Much of Imperial Britain’s foreign policy following the Great War was focused on extracting concessions for oil. Such was also the case with other Western European powers. During the current energy shock, however, most policymakers have used high prices for hydrocarbons as an opportunity to push their countries away from fossil fuels. The Biden Administration’s unprecedented release of oil from the Strategic Petroleum Reserve is representative of such thinking. If this is indeed oil’s “last dance”, then long-term strategic reserves deserve to be depleted in the face of temporary high prices. Governments and capital providers have also clamped down on lending activity in the oil and gas space. Consequently, even as the price of oil broke out to recent highs in 2022, capital is as scarce as it has ever been for oil companies looking to grow production.

The current consensus on petroleum’s future would lead one to believe that investing in anything related to petroleum is a fool’s errand. After all, this is not the 1910s. We are long past concerns about peak oil and are instead being confronted with the prospect of peak demand. That is, of course, assuming the consensus is correct. Are we really in for a sudden drop in oil demand? Is supply really as bountiful as we currently believe?

The component parts of the future of oil demand and supply are far too complex to analyze in this setting, so instead I will leave you with some forecasts. Almost every rational forecaster believes oil demand will increase well into the 2030s as global living standards improve.

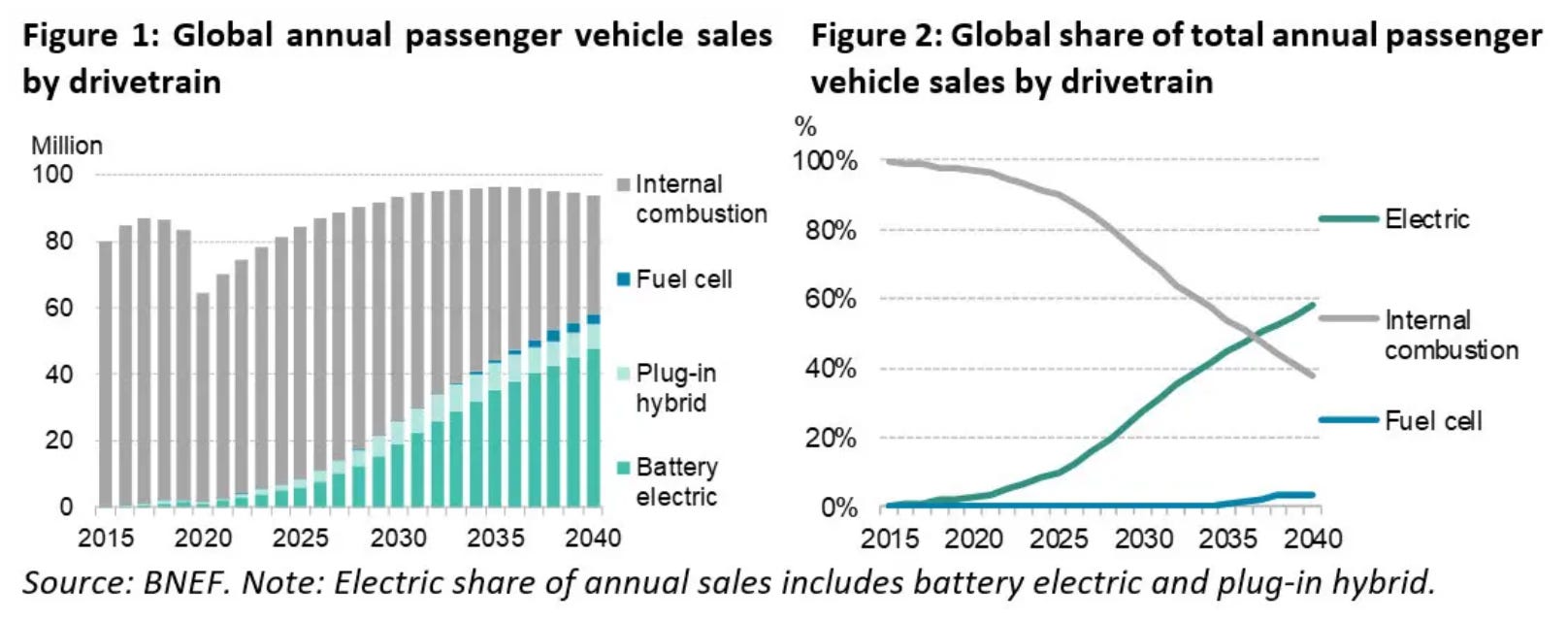

Even the most optimistic forecasts for the widespread growth in electric vehicles show the number of internal combustion vehicles sold increasing rapidly throughout the 2020s before entering an extremely gradual decline.

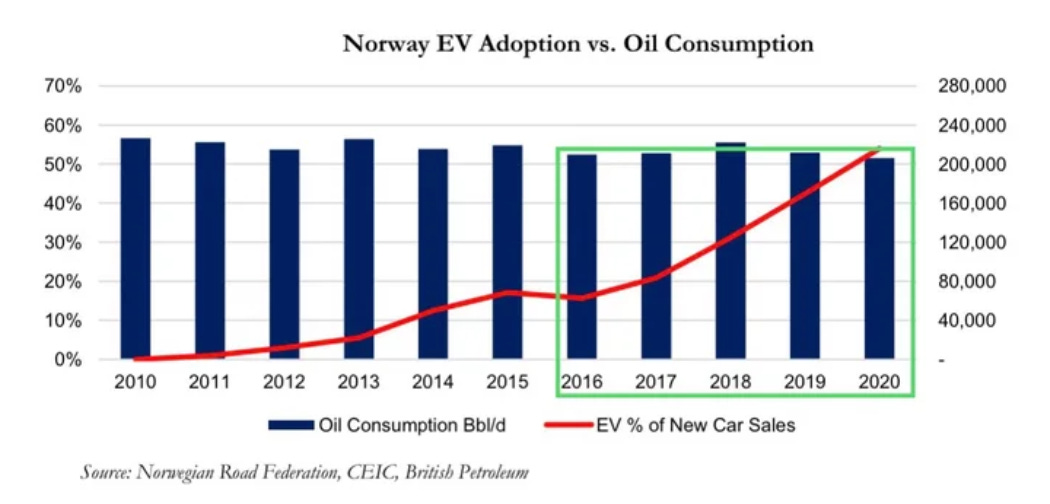

Even if electric vehicles achieve widespread adoption, which is unlikely given resource and practical constraints, there is no guarantee oil consumption will decline. In Norway, where electric vehicles have seen rapid growth, oil consumption has remained relatively stable.

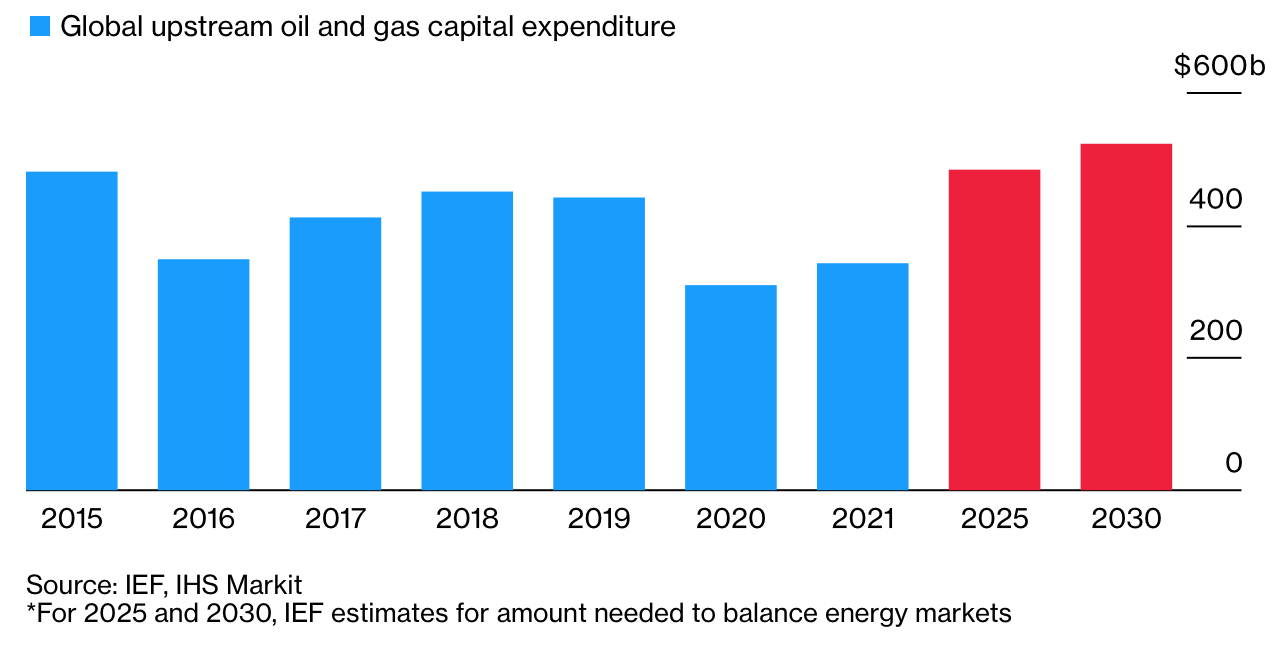

Now let’s look at the supply equation. If we take the low end of the estimates for global oil demand in 2040, which is around 112 mbpd, the world would need to produce an incremental 600 kbpd each year for 20 years. How much capital spending will that take? According to Rystad Energy, we would need $523 billion per year in new capital expenditures to balance the market under less ambitious assumptions for demand.

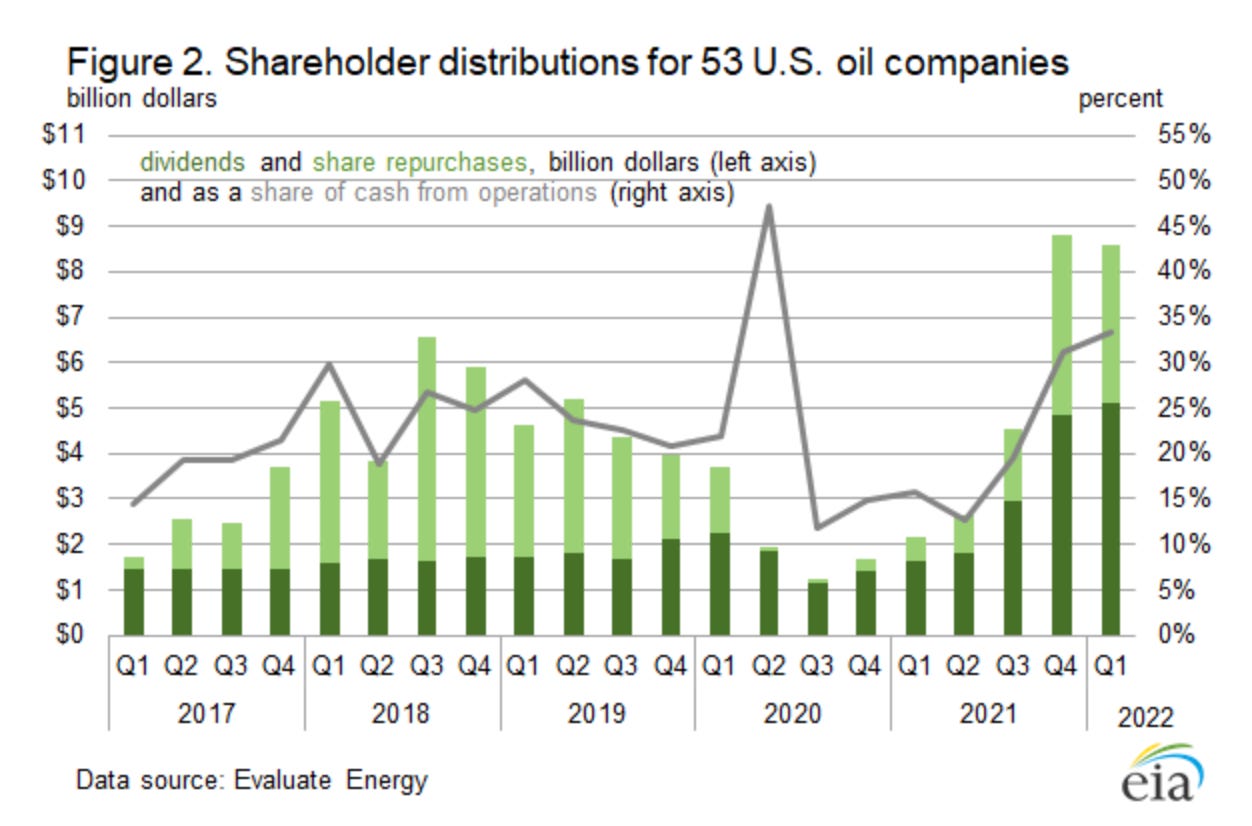

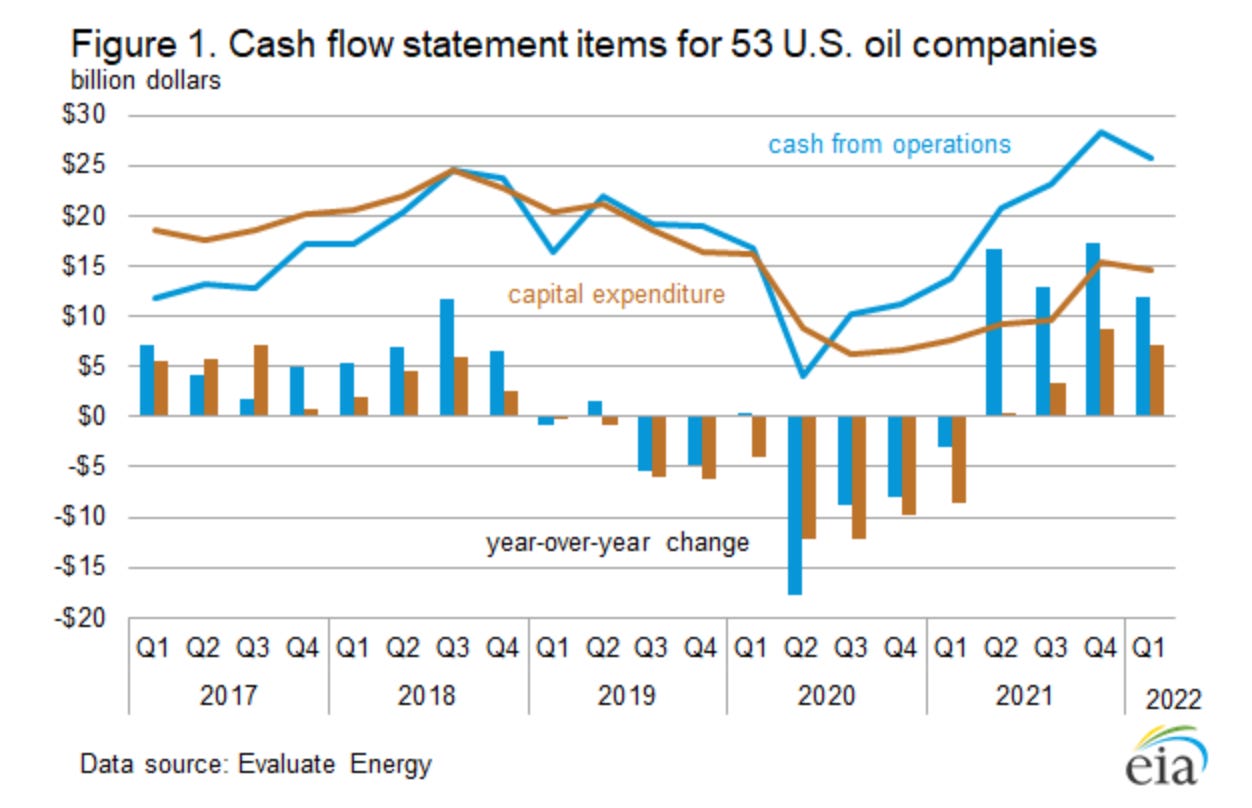

So what is the current capital expenditure situation in the oil and gas industry? In the US, oil companies are increasing the percentage of operating capital returned to shareholders and reducing the amount dedicated to longer-term investments.

Where are new capital expenditures being directed? The data shows it is mostly being plowed into short-cycle shale plays that necessitate high amounts of continued investment to offset steep declines. Meanwhile, long-cycle, low-decline projects are chronically underfunded.

The shale wells that are currently being drilled are also becoming less productive. Thus, capital expenditures on shale will need to increase not to grow aggregate US oil production, but merely to offset potential production declines in the next few years.

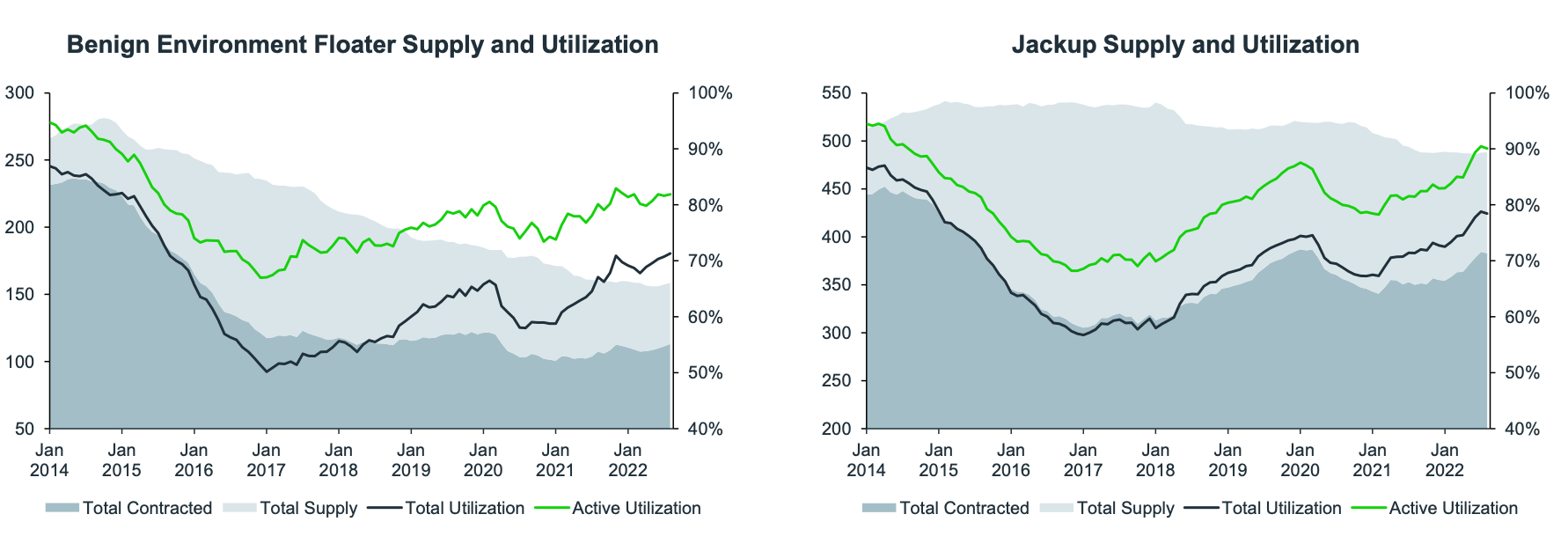

As shale well productivity continues to decline in the coming years, oil companies will likely increase their capital expenditures in long-cycle offshore plays. Unfortunately, following a prolonged bear market, the offshore supply chain has been eviscerated and is incapable of facilitating large supply growth in the next few years.

Finally, OPEC+ will no longer be able to backstop the oil markets if prices begin to threaten global economic stability as underinvestment and larger than anticipated declines kick in. In July alone, OPEC missed its own production quota by a remarkable 3.8 mbpd.

This is all to say that the current consensus is dramatically wrong. Though it could not be perceived more differently, the fundamentals of the oil market in 2022 much more closely resemble that of 1914 than most suspect. While we have not reached “peak oil,” the marginal barrel will continue to get more expensive to extract as short-cycle plays are exhausted. Similarly, the current petroleum demand outlook is robust, even if not driven by the proliferation of any one new technology but by the continued economic advancement of all nations.

There is one key difference worth noting that could make the 2020s bull market far more extreme than that of the 1910s. As oil steadily increased in price from 1914 onwards, it was not just oil companies that reacted aggressively to price signals, but governments as well. The situation could not be more different today. Most OECD nations have dedicated themselves to reducing the supply of oil by either prohibiting it outright or making its extraction significantly more costly. The net effect is a severe distortion of price signals that is reducing the ability of producers to balance the oil market. If the 1914 to 1920 timeframe is any indicator, oil prices need to go substantially higher from here to trigger a multi-year supply response capable of balancing the market.

(For a more detailed look at current supply issues, check out my July analysis:)

Sources:

https://www.reuters.com/business/energy/falling-spare-oil-capacity-underscores-need-more-investment-iea-says-2021-10-14/

https://www.sciencedirect.com/topics/earth-and-planetary-sciences/giant-oil-field

https://energyindustryreview.com/analysis/pros-and-cons-revival-time-for-oil-and-gas-industry/

https://www.goldmansachs.com/insights/pages/from-briefings-20-january-2022.html

https://energyeducation.ca/encyclopedia/Hubbert%27s_peak

https://www.mdpi.com/1996-1073/7/12/7955/htm

https://pubs.acs.org/doi/pdf/10.1021/bk-2010-1032.ch001

https://www.sciencedirect.com/science/article/pii/S2666049022000524

“The present status of the oil shale industry" 1921, Colorado School of Mines Quarterly, Apr. 1921, v.16 n.2 p.12.

https://profitworks.ca/blog/358-john-d-rockefellers-business-strategy-net-worth-analysis-and-his-secret-to-success

https://thedriven.io/2020/05/19/covid-19-a-bump-in-the-road-for-ev-growth-ice-cars-still-on-road-to-nowhere/

https://www.bloomberg.com/news/articles/2021-12-07/oil-gas-investments-must-rise-to-523-billion-a-year-says-ief?leadSource=uverify%20wall

https://s23.q4cdn.com/956522167/files/doc_presentations/2022/09/Investor-Presentation_September-2022.pdf